Thailand’s light vehicle market recorded 201,247 registrations in Q1 2026, marking a 20.3% year-on-year increase from 167,283 units in Q1 2025, the sharpest quarterly rebound recorded since the market contraction of 2024. The recovery was driven by a convergence of structural and policy forces: accelerated EV deliveries ahead of the EV 3.0 incentive deadline, carry-over booking momentum from Motor Expo 2025, and sustained interest in electrified powertrains amid volatile fuel prices. For OEMs and distributor networks operating in Thailand, this quarter signals both a volume recovery and a fundamental shift in the competitive order that will require revised product positioning and network investment strategies.

Executive Summary

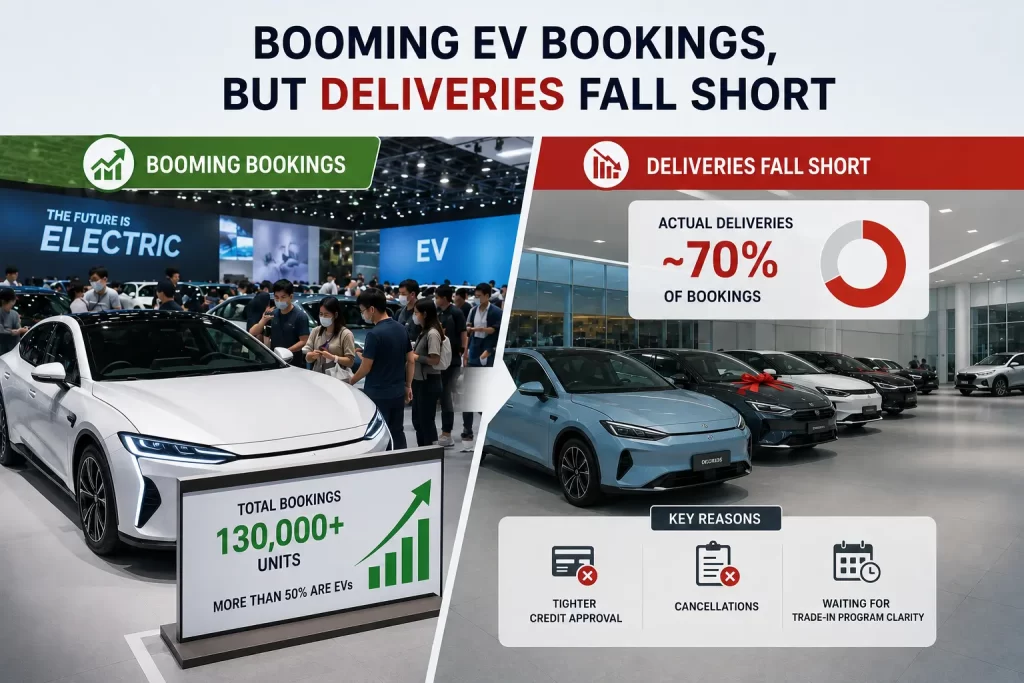

- Thailand registered 201,247 light vehicles in Q1 2026, up 20.3% YoY, with January alone accounting for 92,500 units driven by EV 3.0 delivery acceleration.

- Toyota retained market leadership at 34.21% share (68,842 units), though its YoY growth of 5.0% was outpaced significantly by Chinese brands entering at scale.

- BYD rose to Rank 4 with 14,164 units (+61.7% YoY), while Jaecoo delivered the market's most disruptive entry at 10,620 units, up from 501 units in Q1 2025, a 2,020% YoY increase.

- The Passenger Car (PC) segment surged 33.0% YoY to 155,471 units (77.3% share), while LCV contracted 9.3% (a structural reversal of Thailand's traditionally pickup-dominant market).

- EV and HEV combined now represent 52.0% of total registrations, signaling a tipping point in powertrain transition that OEMs without electrified portfolios cannot afford to ignore.

Market Overview: Q1 2026 Registration Performance

Thailand’s Q1 2026 volume was shaped by an uneven monthly distribution. January recorded a disproportionately high 92,500 units as automakers and dealers rushed EV deliveries to qualify under the EV 3.0 subsidy framework, which offered import duty and excise tax reductions for compliant models. February normalized to 48,994 units before a moderate recovery to 59,753 units in March, reflecting underlying demand stabilization.

Tightened hire-purchase and leasing credit standards, introduced by the Bank of Thailand from late 2025, constrained volume in the non-bank financing segment, particularly affecting mass-market ICE models and LCV buyers. This regulatory headwind disproportionately impacted the pickup and commercial segment, contributing to the LCV contraction observed across the quarter.

Brand Performance: Top 5 Rankings Q1 2026

Toyota extended its dominance with 68,842 units and a 34.21% market share, though its 5.0% YoY growth rate was the lowest among the top five, reflecting a portfolio mix still weighted toward ICE and HEV rather than BEV, the fastest-growing fuel category. Honda held second position at 22,619 units (+2.3% YoY), maintaining stability without meaningful share gain. Isuzu declined 7.6% to 20,168 units, consistent with the broader LCV contraction as credit tightening and softening commercial demand compressed the pickup market.

The competitive story of Q1 2026 belongs to Chinese brands. BYD consolidated its fourth-place position with 14,164 units (+61.7% YoY), reinforcing its role as the dominant EV-native competitor to Japanese incumbents. More significantly, Jaecoo emerged as the market’s most disruptive new entrant, delivering 10,620 units in Q1 2026 from a base of just 501 units in Q1 2025 (a 2,020% YoY increase) that elevated the brand from Rank 26 to Rank 5 in a single quarter. This trajectory, if sustained, positions Jaecoo as a direct volume threat to Isuzu and Honda before year-end.

| Rank | Brand | Q1 2026 Units | Market Share | YoY Change | Strategic Note |

|---|---|---|---|---|---|

| 1 | Toyota | 68,842 | 34.21% | +5.0% | Dominant share, but low growth rate signals vulnerability to EV-native challengers |

| 2 | Honda | 22,619 | 11.24% | +2.3% | Holding position without momentum; electrification pace is the key watch indicator |

| 3 | Isuzu | 20,168 | 10.02% | -7.6% | LCV decline reflects structural headwind; credit tightening compounds pressure |

| 4 | BYD | 14,164 | 7.04% | +61.7% | Fastest-growing top-5 brand; EV portfolio directly aligned with policy incentives |

| 5 | Jaecoo | 10,620 | 5.28% | +2,020% | Most disruptive Q1 entry; Rank 26 to Rank 5 in 12 months signals serious network scaling |

Segment Breakdown: PC Rises, LCV Contracts

The PC segment’s 33.0% YoY expansion to 155,471 units (77.3% of total market) marks a structural departure from Thailand’s historic profile as a pickup-dominant market. This shift reflects the combined effect of new EV and HEV model launches, overwhelmingly concentrated in the passenger car body style, and reduced commercial vehicle demand amid tighter credit conditions. LCV registered 45,675 units in Q1 2026, a 9.3% YoY decline representing 22.7% of total volume. The contraction is consistent with patterns observed in the second half of 2025 and is unlikely to reverse sharply until hire-purchase credit standards loosen or a new cycle of commercial fleet renewal emerges.

Powertrain Transition: EV and HEV Cross the 52% Threshold

The powertrain composition of Q1 2026 registrations confirms that Thailand’s electrification transition has passed a critical inflection point. EV and HEV combined accounted for 52.0% of total volume: a threshold that, once crossed, typically accelerates further adoption as charging infrastructure, resale confidence, and financing availability improve in parallel.

EV registered 57,108 units, up 120.5% YoY, representing 28.4% of total market volume. The January concentration of this figure warrants attention: a significant portion of Q1 EV volume reflects dealers and importers accelerating delivery schedules to capture EV 3.0 subsidy eligibility before the policy window closed, rather than organic Q1 demand. HEV reached 47,505 units (+29.8% YoY, 23.6% share), driven by Japanese OEM hybrid portfolio strength and growing preference for electrified options without charging dependency. Diesel declined 3.6% to 30.3% share, and Petrol contracted 16.4% to 15.2% share.

For a full breakdown of Thailand’s powertrain shift by fuel type and brand trajectory, see: Thailand EV Registrations Surge 120.5% in Q1 2026: Policy-Driven Spike or Structural Shift?

Analyst Note

The 20.3% YoY rebound in Q1 2026 should be interpreted with structural nuance rather than taken as a clean demand recovery signal. January’s 92,500-unit spike was driven materially by EV 3.0 deadline dynamics, not by a sustained shift in underlying purchase intent. OEMs and distributors that plan Q2 and Q3 inventory allocation based on Q1 headline volume risk significant overcommitment. The more durable signal in this quarter’s data is Jaecoo’s ascent from Rank 26 to Rank 5 in 12 months: this reflects a maturing Chinese brand distribution infrastructure in Thailand that will structurally compress the competitive space for mid-tier Japanese models in the 2026 to 2027 planning horizon. Combined with BYD’s continued volume build, Chinese OEMs now command approximately 12.3% of the total market from a near-zero base three years prior.

Strategic Implications

| Audience | Key Implication | Priority Action |

|---|---|---|

| OEMs | EV 3.0 closure creates Q2 demand normalization risk for BEV-heavy model mixes; HEV's organic 29.8% growth offers a more stable near-term volume driver | Reassess Q2 to Q3 allocation plans against post-incentive demand levels, not Q1 delivery volumes |

| Distributors | Jaecoo's 2,020% surge signals Chinese brand distribution networks have crossed a scaling threshold in B-SUV and C-SUV segments | Reassess competitive positioning and dealer incentive structures before mid-year review cycles |

| Dealer Networks | PC at 77.3% of total volume vs. LCV contraction creates a showroom traffic imbalance; provincial pickup-oriented locations face a growing coverage gap | Evaluate portfolio mix and location strategy against shifting urban and suburban PC demand |

| Market Analysts | January's 45.9% share of Q1 total distorts standard quarterly trend analysis; YoY comparisons for Q2 2026 must account for the EV 3.0 base effect | Use Proliance's monthly province-level database for clean trend modeling free of policy-event distortion |

Outlook

Q2 2026 registrations are expected to normalize materially following January’s EV 3.0-driven spike, with monthly volumes likely stabilizing in the 55,000 to 65,000 unit range absent new policy stimulus. The key variable to monitor is whether EV demand sustains momentum on organic market fundamentals once subsidy support recedes, particularly as the EV 3.5 framework takes shape. The Bank of Thailand’s continued oversight of hire-purchase credit standards represents the primary downside risk for LCV and mass-market ICE volume recovery. For OEMs tracking competitive dynamics, Jaecoo’s Q2 registration performance will serve as an early signal of whether its Q1 volume reflects structural market penetration or a concentrated delivery catch-up. Proliance will publish updated province-level registration data for Q2 2026 as figures are confirmed.

Access the Full Dataset

This analysis is based on Proliance’s vehicle registration database covering Thailand at province level. To request a data sample or discuss coverage for your market intelligence needs:

Proliance Company Limited — Critical Data for Critical Decisions

References

- Bank of Thailand, Monetary Policy Report and State of Thai Economy, January 2026. bot.or.th

- Thailand Board of Investment, Thailand Updates EV3 / EV3.5 Incentives to Strengthen Position as Regional EV Hub. thailand.go.th

- The Nation Thailand, Thailand Automotive Industry Coverage, Q1 2026. nationthailand.com